Gary Shawhan, Contributing Editor

The CHEMARK Consulting Group

“Buyer beware” is a catch phrase that has meaning for most of the activities that accompany everyday life. In the M&A process, this can work the other way as well- “Seller beware”. In the CASE markets, as with most markets, the range of scenarios that accompany any M&A activity are both varied and individual to the actual situation.

In Part 1 of the article- “Understanding the Dynamics for Buyers and Sellers”, we explored a variety of issues that present themselves during the M&A process. In Part 2 of this article we will consider the benefits for accessing outside consulting services or advisors as part of the process.

Engaging outside services to assist in the M&A process is something that should be considered by buyers or seller when contemplating a merger, acquisition or divestiture. The values for accessing outside services vary widely depending on the size and resources available within the company to support the effort.

In the case of large, global companies with complex organizations, the value of outsider assistance is often greatest during the evaluation of candidate companies and then during courtship. With small to mid-sized companies and for private equity firms involve in mid-market to smaller size company acquisitions, the value of engaging outside consultants or advisors typically extends throughout the M&A process. The importance and value of the services needed varies significantly, however, based on the specifics of the situation.

While the benefits of including outside consultants/advisors are many, comments in this article are especially directed toward mid-market to smaller-sized companies.

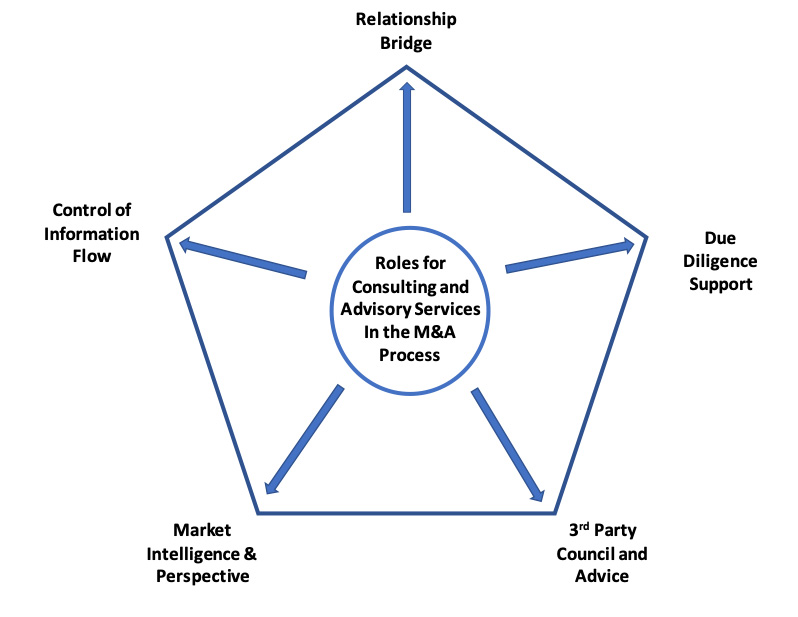

Figure 1 highlights 5 important elements of the M&A process where outside services play a valuable role in assisting or providing support to buyer or sellers during mergers, acquisitions or divestitures.

Figure 1: 5 Values for Accessing Outside Services during the M&A Process

Relationship Bridge

Successful negotiations rely on the establishment of effective communications between the buyer and seller. Achieving understanding and trust (between both buyer and seller) is an essential part of this process. In most cases, this is a goal that requires dialogue on various issues important to each party and the willingness to consider and take into account the others point-of-view.

Company culture and organizational practice variations represent a common area which can evolve into misunderstanding or conflicts between buyer and seller. In a direct B2B scenario, these differences can easily become an impasse to further discussions. Identification of the issues that can become potential conflicts between the two parties (early in the M&A process) is very important. Proactive efforts to resolve these issues and can make the difference in achieve a successful end result.

One of the benefits of accessing outside services, early in the M&A process, is to provide a buffer between the buyer and seller to help sort out potential areas of conflict. In these cases, the role of a consulting firm is to provide suggestions for compromise or offer a better understanding to the buyer or the seller of the reasoning behind the other party’s point-of-view.

Identifying and understanding the needs of the ownership of the company that is to be acquired is critical. Early in conversations between the buyer and seller each have identified targets and goals. It is unusual for there to be agreement on most of the things each party is looking for from the process. A key value provided by outside consulting services is to work through the discovery process and provide a forum for compromise on those elements that make sense and bring both parties closer together in their expectations and goals for the acquisition.

Control of Information Flow

There are a variety of reasons that control of information passing between the buyer and seller needs to be controlled and protected. These situations include the following general categories:

Table 1: Important Elements of Information Transfer during M&A Activities

- Secrecy during the M&A Process

- Employee awareness

- Customer Awareness

- Competitor Awareness

- Market/Industry Awareness

- Protection of Business Information

- Transfer of Financial Data

- Sharing of confidential Market/Customer Data

- Formulations; Trade Secrets, Proprietary

- Manufacturing, Operational Details

- Other

Secrecy during the M&A Process

From the start of any conversation about the possibility of an acquisition (or divestiture) confidentiality is a key requirement. Since there is no certainty about the final outcome, awareness of such on-going discussions beyond the select few involved in the process can have damaging and irreversible consequences.

One of the most important roles for outside consulting services is to provide a funnel for communications between the two parties. Limiting the number of individuals in both organizations that are involved in the process and then working through a 3rd party to facilitate the transfer of information between the buyer and seller is extremely important. Third party participation provides a valuable level of control in information flow during the process.

Employees, primarily on the “seller’s side”, who become aware of an on-going effort by owners to sell the business become concerned about their future. Some key people may leave the company prematurely or consider leaving well before an action is actually taken. Morale can also suffer as rumors spread throughout the organization. Generally speaking, these rumors normally have little to do with what is actually being considered by management. Unfortunately, they can result in irreparable damage to the company.

Customers, suppliers of raw materials, equipment or companies providing services to the business including distribution, field reps, etc., may also react to such rumors prematurely in ways damaging to the company. Customers can consider protecting their market position by engaging alternative sourcing options. Companies that rely on their business relationship with the company they feel may be acquired may realign themselves with competitors.

Competitors, who become prematurely aware of such activities, will see the situation as an opportunity to target the company’s customers. This includes spreading rumors in the marketplace that cast uncertainty and concern about the company as a future source of supply. Implications of instability and/or uncertainty about the future of the company as a reliable supplier can result in long-term damage to its reputation. The consequence can be a loss of market share.

Protection of Business Information

The sharing of business information and the transfer of key financial reports and records is a critical activity during the M&A process. Control of the process for sharing this information by sellers to perspective buyers is necessary. It also needs to be managed. Only those individuals that are involved in the discussions about a possible acquisition of the business and need to have access to this information.

Accountability by the recipient, to protect the financial data and business information of the seller is often better served by having outside, intermediary consulting services manage and monitor the transfer of financial data throughout the process. In addition, follow-up questions normally result and/or requests for additional information evolve throughout the process. Third parties provide a valuable service while keeping these communications separate from the company’s day-to-day business activities.

Since it is likely that some of the perspective buyers are either direct competitors or involved in the market space served by the seller. Market and strategic information important to the future of this business being acquired needs be carefully managed. This includes limiting the sharing of key business information until it is required to move discussions to the next step.

Intellectual property including proprietary formulations and other trade secret information must also be protected. This includes manufacturing process information which give the seller a competitive advantage over others in the marketplace. Outside consulting services or advisors offer an important support function by ensuring this information is not exchanged during the process unless it becomes absolutely necessary to move negotiations toward deal closure.

3rd Party Advice/Opinion

Having a sounding board for discussions of next steps in the process is one of the benefits of employing an outside advisor. Independent viewpoints from those with other experiences in M&A activities bring a valuable dimension to the process. While internal company advisors and their opinions are often helpful and useful, the reality is that they come from the same business culture.

Whether buyer or seller, working through the process of bringing two companies together, understanding and identifying key areas for compromise that can move both parties closer together (as opposed to moving further away) is key to successful negotiations.

Electing to use outside consulting services to pinpoint and work through various potential areas of conflict is an important consideration. The benefits for having a third party gather information from both sides on a particular issue and then being able to look at it with objectivity is one of the most valuable contributions made by consultants/advisors involved in supporting the M&A process.

Market Intelligence & Perspective

Early in this process there are important elements of planning and preparation that need to be addressed by either the seller or the buyer. On the seller side, identifying key features of the business that can contribute positively to its valuation by perspective buyers is very important. These items often include: Brand and brand strength: geographic market reach; market share and/or strength in certain segments; support resources that are in place such as sales, technical service or R&D; proprietary information technology (IT); and others.

In positioning the company for maximum value, there is an advantage in having an outside viewpoint and perspective on the relative values that are contained within the company as they specifically relate to an individual perspective buyer. Highlighting the uniqueness of the business as well as identify those elements which may compromise its value (at the outset of the process) is an important exercise in achieving this end. Third party involvement through consultants/advisors is tactically very useful for this purpose.

From a seller’s standpoint, a second benefit for engaging third party assistance in the M&A process is to obtain a broader view of possible buyers for this business. In today’s marketplace, the better business fit is not necessarily with direct competitors. It can be, for example, with companies serving the same customer base but with other products. These companies are looking to extend their product portfolio and provide a more complete line of product solutions.

Market diversification, extension of geographic market reach or strengthening their overall profitability by adding new, novel products which are more profitable, or short-cutting the length-of-time required to implement greenfield growth plans represent other drivers favoring a growth strategy through acquisition. In all the above cases, the inclusion of a third party adds vision and increases the opportunities for bringing a broader list of candidate buyers to the table.On the buyer side, when contemplating an M&A effort, third party participation extends the list of potential candidate targets that conform to the criteria that they have set. In addition, as noted earlier, outsider services can provide a buffer and sounding board during the process to bring sellers and buyers close together.

Due Diligence Support

In mergers and acquisitions, buyers own the responsibility for protecting their company from making a “bad deal” by doing in-depth analysis of all aspects of the sellers’ business. This process is referred to as due diligence.

There are many elements in the due diligence process including those listed in Table 2. The level of important and complexity involved in doing an acceptable and thorough assessment in each of these areas will vary widely and be individual to the specific buyer/seller circumstance.

Depending on the size and nature of the business to be acquired, emphasis placed on the individual items listed in Table 2 (during the due diligence process) can vary significantly. The need to do a thorough job in financial analysis of the seller business is common to any perspective M&A process. Accounting practices including consideration of software and hardware compatibility issues deserves special attention. These items, if not sorted out ahead of time, can significantly complicate the ease at which a smooth transition can be achieved following completion of the acquisition.

In today’s marketplace, the challenges to the buyer represented by the areas of human resources, environmental compliance and regulatory compliance are a top priority since they all can bring risk and, in some cases, irreparable damage to the buyer. Depending the size of the acquiring company and the availability of resources with expertise in each of these field to do a thorough job, these are all areas where outside advisor/experts are needed to insure all the bases are covered before closing on any business agreement.

Table 2: Important Elements to be Addressed as part of Due Diligence

- Finance

- Financial records and metrics

- Projections, realistic expectations going forward

- Computer software compatibility and business record keeping methodology

- Human Resources

- Health care plans

- Employee compensations, incentive & benefit plans, retirement plans

- Company policies

- Environmental Issues, Compliance

- Liabilities (or pending issues) related to clean-up/reclamation of properties (owned or leased)

- Regulatory Compliance

- Government agencies compliance

- Pending or potential future regulatory issues related to the company or its products

- Outstanding Contract/Business Obligations

- Union presence

- Supplier contracts or customer contractual obligations

- Litigations (current or pending), Legal issues, Labor disputes

For larger mergers or acquisitions involving global corporations, there is an M&A team in place that follows an established set of criteria for evaluating potential acquisitions. Once negotiations reach the point where an offer is expected to be made, this group takes ownership of the due diligence process. Outside consulting assistance or the use of industry advisor/experts are selectively brought into the process as requested by the buyer.

In the case of mid-market to smaller sized company acquisitions the business dynamics can change considerably when entering into due diligence. Internal resources vary widely in these situations and the breadth of the experience by the buyer often dictates the need for additional outside services or specific experts to assist in the completing of the due diligence process. This situation applies to both medium to smaller-sized companies as well as to private equity firms.

In the case of private equity firms, the need for outside consulting services or advisors during due diligence varies with the experience of their existing team in the market(s) where the target company participates. It also varies with the internal expertise in the various elements of due diligence that need to be carried out to complete the M&A process. Complimenting and augmenting the available resources present at the private equity firm is a role often served through outside consulting services.